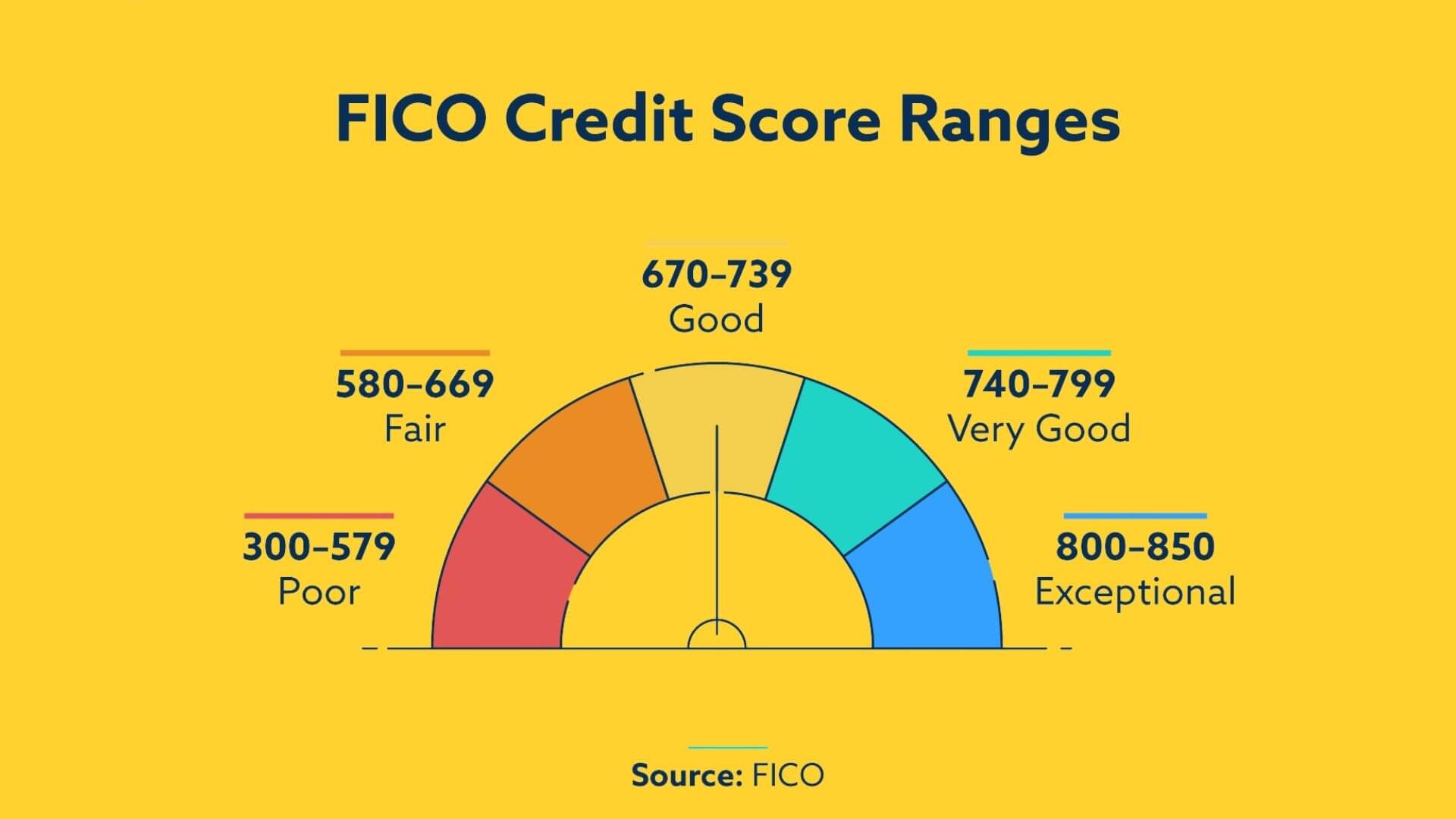

Multiple loan applications can adversely impact your credit score. Each loan application is visible in your credit file. It stays there for two year. The loan remains on your credit record forever if it is not repaid. You should not apply for credit multiple times. Late payments and rate-shopping also negatively impact your credit score.

Rate-shopping impacts your credit rating

It is crucial to shop around for the lowest interest rates when applying for large loans, such as a mortgage and a car loan. There are some rules that you should follow in order to preserve your credit rating. If you do not follow these rules, you could end up reducing your credit score in the end.

First of all, you should try to shop around for rates before making the first application. Doing this will help you avoid multiple applications being submitted at the same time. This will prevent multiple inquiries from impacting your credit.

Hard inquiry affects your credit rating

It's possible to wonder how hard inquiries impact your credit rating, especially when you apply for loans. Good news is that hard inquiries have very little impact on your credit rating when applying for loans. Credit experts say that a hard inquire will not reduce your credit score by more than a few points. The number of hard inquiries you have on credit reports and your credit score will determine how many points you lose.

An inquiry that is considered a hard inquiry can be found on your credit history for two years. Hard inquiries won't affect you score right away but will remain on your credit report for up to two years. Unauthorized inquiries can be disputed at a credit dispute centre. Unauthorized hard inquiries may result from a lender pulling your credit reports without your permission or identity theft.

Late payments affect your credit rating

Late payments on credit card and loan accounts can impact your credit rating. This can be avoided by paying off a debt as soon as it becomes due. Late payments can negatively impact your credit score. It is best to pay an overdue account off within 30 calendar days. If you are unable to pay the account in time, your credit score may be affected.

Credit scores are calculated using a number of factors to determine if someone is able or not to repay debts. Payment history accounts for as much as seven years. A late payment can reduce your score by up 100 points. The impact on your credit score will be less if it is already low. An individual can be forced to miss a payment because of financial emergencies like job loss. This is why you should seek help and strategies for resolving the situation.

Avoiding a hard inquiry

Knowing how hard inquiries affect credit scores is the first step in avoiding an inquiry when applying to for loans. While each inquiry does impact your score, there are several ways to minimize the impact. Avoid applying for loans until you are certain you will be approved. A pre-qualification service is offered by lenders. It does not require you to complete a hard inquiry. This will help you determine if you are eligible for a loan.

You can avoid hard inquiries by only applying for one type loan at a given time. A single hard inquiry will generally lower your score by a few points. However, if you have multiple inquiries in a 12-month time period, the impact can be even more severe. Fortunately, there are other forms of credit inquiries that do not impact your score. In some cases, prospective employers may conduct soft inquiries during employment screenings. However, before you allow your prospective employer to conduct a soft inquiry, you should obtain your consent in writing.

A personal loan can increase your credit score

While you may be concerned about your credit score, it is actually possible to improve it by taking out a personal loan. Because it lowers credit utilization, this type of loan can help improve your credit score. Your credit score is based on this ratio, and many people have high credit utilization ratios. To improve this ratio, it is important to keep your credit card bills low and to not max out your cards.

You can also improve your credit score by paying off any outstanding balances. This will help you look more trustworthy and reduce your credit card bill. The only problem with this strategy is that it may lead to you accumulating more personal loan debt.